In 2025, the wealthiest people you know might not be driving luxury cars or living in mansions. As traditional symbols of success fade in importance, a profound shift is redefining the very concept of wealth in our society. The gleaming sports car and sprawling estate—once the ultimate markers of prosperity—have been dethroned by less tangible but more meaningful measures.

Yet many of us remain trapped in outdated wealth definitions, measuring our success against material yardsticks from another era. This misalignment creates a peculiar modern dilemma: financial achievement without fulfillment, accumulation without satisfaction. The anxiety that comes from chasing the wrong wealth metrics leads to chronic dissatisfaction and priorities that don’t actually enhance our lives.

This article provides a comprehensive framework for understanding what true wealth really means in 2025, backed by current research from Charles Schwab’s Modern Wealth Survey and insights from financial experts who’ve tracked this evolution. You’ll discover the multidimensional nature of modern prosperity—where time freedom, experiences, health, relationships, purpose, and yes, financial security—create a more holistic wealth definition.

The Financial Paradox of 2025: Earning More, Having Less

You’re making more money than your parents did at your age, yet you can’t afford what they could. This strange reality hits many people today. Your paycheck looks bigger on paper, but it buys less at the store.

Prices for everyday items have shot up faster than wages. This gap creates real stress when you look at your bank account. Many people feel they’re working harder than ever but falling behind anyway.

Tips:

- Compare your salary to what your parents made at your age, then adjust for inflation using online calculators

- Track how much of your income goes to necessities versus what your parents spent

- Remember that feeling financially squeezed isn’t your fault – it’s a widespread economic trend

- Consider how inflation has affected different spending categories differently (housing vs. electronics)

- Look for ways to maximize your purchasing power through strategic spending

The Housing Crisis: Why Your Parents Bought a Home for 2x Their Salary While You’re Looking at 5-7x Yours

Buying a home today costs much more compared to what people earn. Your parents likely bought their first house for about twice their yearly income. Now you’re looking at prices that are five to seven times what you make in a year.

This massive jump makes homeownership feel impossible for many. Add in today’s higher mortgage rates, and monthly payments become even more painful. The gap between incomes and home prices keeps growing, pushing the dream of owning a home further away for many people.

Tips:

- Look at housing costs in different areas – sometimes moving just 30 minutes away can cut prices dramatically

- Consider house-hacking options like buying a duplex and renting half to offset your mortgage

- Save aggressively by automating transfers to a dedicated home down payment fund

- Explore first-time homebuyer programs that offer lower down payment requirements

- Remember that renting isn’t “throwing money away” if it allows you to live in an area with better job opportunities

The Crushing Weight of Education: How Student Loan Debt Changed the Game

College costs have exploded while wages haven’t kept pace. Your parents might have worked summer jobs to pay for school, but that’s impossible today. Many young adults now start their careers owing tens of thousands in student loans.

These monthly payments eat into money that could go toward buying homes or saving for the future. The burden changes how people plan their lives – from delaying marriage to choosing careers based on pay rather than passion. Student debt has become a ball and chain that follows many people for decades.

Tips:

- Explore income-based repayment options if your student loan payments exceed 10% of your income

- Look into loan forgiveness programs for public service work or certain professions

- Consider refinancing private loans when interest rates drop

- Pay a little extra on principal when possible to shorten the life of your loans

- Don’t neglect retirement savings while paying off student debt – try to do both

Healthcare: The Silent Budget Killer Your Parents Didn’t Face

Healthcare costs bite into your budget in ways your parents never experienced. Insurance premiums, deductibles, and copays take a bigger chunk of your paycheck each year. Even with insurance, a single hospital stay can lead to thousands in bills.

Many people avoid getting care they need because they worry about costs. These rising expenses force tough choices between health and other needs. The stress of medical costs adds another layer to financial anxiety that previous generations didn’t face to this degree.

Tips:

- Maximize your HSA if you have a high-deductible plan – it offers triple tax advantages

- Always review medical bills for errors – they’re surprisingly common

- Ask about cash prices, which can sometimes be lower than using insurance

- Look into prescription discount programs like GoodRx even if you have insurance

- Budget for healthcare as a major expense category, not just an occasional cost

Lifestyle Inflation and Modern Necessities: The Subscription Economy

Your monthly budget now includes many items your parents never had to pay for. Cell phone bills, internet service, and streaming subscriptions add up quickly. Many of these services feel essential for work and social connection today.

Each subscription might seem small on its own, but together they create a constant drain on your finances. The pressure to stay current with technology adds another layer of expense. These modern necessities create a new baseline of spending that wasn’t part of your parents’ budget.

Tips:

- Audit all your subscriptions quarterly – cancel ones you haven’t used in the last month

- Share subscription costs with family members where possible

- Look for bundle deals that combine services at lower rates

- Try the “one in, one out” rule – for every new subscription, cancel an existing one

- Consider whether each digital service truly improves your life or just consumes time and money

The Shrinking Safety Net: How Traditional Support Systems Have Changed

The financial protections your parents counted on have largely disappeared. Pensions that guaranteed retirement income have been replaced by 401(k)s that shift risk to you. Job security has weakened, with fewer people staying at one company for their whole career.

Benefits like health insurance cost more and cover less than they used to. Government programs that once helped the middle class have been cut back or haven’t kept up with needs. These changes mean you face more financial uncertainty than previous generations did.

Tips:

- Take full advantage of any employer match in retirement accounts – it’s free money

- Build your own safety net with an emergency fund covering 3-6 months of expenses

- Develop multiple income streams to protect against job loss

- Research what government benefits you qualify for – many people miss out on programs they’re eligible for

- Consider joining professional organizations that offer group insurance rates or other benefits

Taking Control: Actionable Strategies for Financial Wellness in 2025

You can still build financial security despite these challenges. Start by tracking where every dollar goes and cutting spending on things that don’t truly matter to you. Pay yourself first by automating savings before you can spend the money.

Look beyond traditional paths – house hacking, side businesses, and skill development can all boost your financial position. Focus on increasing your income through strategic career moves or additional work. Small, consistent steps add up over time. Taking control of your money situation brings both financial benefits and peace of mind.

Tips:

- Follow the 50/30/20 budget: 50% for needs, 30% for wants, 20% for savings and debt payoff

- Invest early and often, even small amounts, to harness the power of compound growth

- Develop valuable skills that command higher pay in the marketplace

- Create a clear financial plan with specific milestones and celebrate when you reach them

- Find a financial accountability partner to help you stay motivated and on track

- Remember that financial wellness isn’t just about money – it’s about creating the life you want

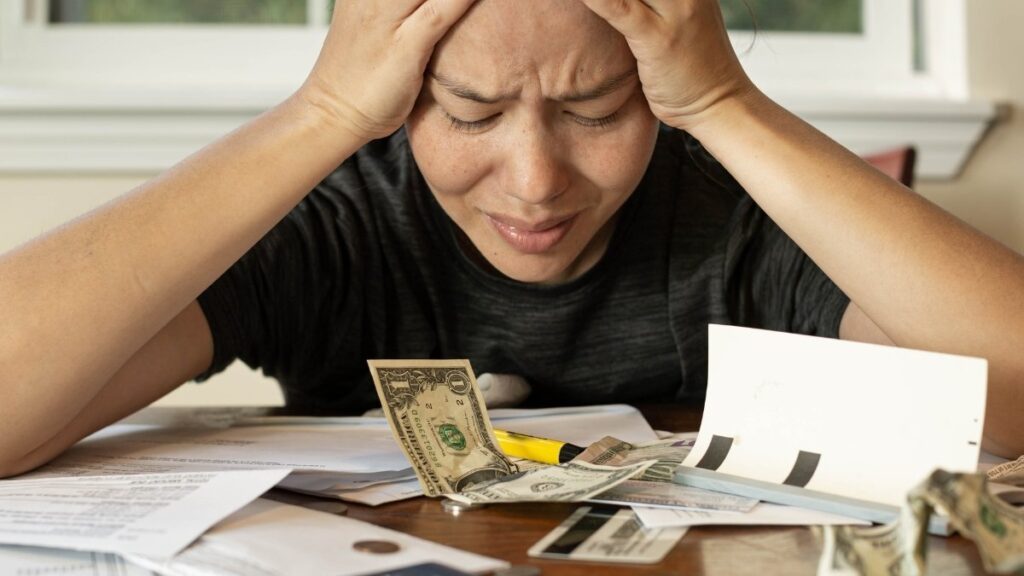

The Psychological Toll of Financial Stress in 2025

Money worries don’t just hurt your wallet – they hurt your health too. Recent studies show that most Americans feel stressed about money, with younger people hit hardest. This constant worry changes how your body works, raising stress hormones and blood pressure.

Your brain gets stuck in survival mode, making it harder to plan for the future. Many people lose sleep, feel on edge, or struggle to focus at work. These mental effects can lead to poor money choices, creating a cycle that’s hard to break. Financial stress isn’t just about numbers – it’s about your wellbeing.

Tips:

- Set aside 10 minutes daily for mindfulness practice to break the stress cycle

- Create a “worry time” where you address financial concerns, then put them aside

- Connect with others facing similar challenges through support groups

- Use apps that track your mood alongside your spending to spot emotional patterns

- Break big financial problems into smaller, manageable steps to reduce feeling overwhelmed

- Talk to your doctor if financial stress is affecting your sleep or physical health

The Widening Wealth Gap: How Asset Inequality Amplifies Income Differences

Having assets – not just income – makes all the difference in building wealth. While your paycheck helps you live, assets like homes, investments, and businesses create more money while you sleep. This gap shows up clearly across different groups in America. White families are much more likely to get an inheritance than Black or Hispanic families.

This head start compounds over time, as money makes more money. The wealth gap grows much faster than income differences alone would suggest. This pattern makes it harder for many people to catch up, no matter how hard they work.

Tips:

- Start building assets as early as possible, even with small investments

- Look into first-generation homebuyer programs if your family doesn’t have property wealth

- Join investment clubs or communities focused on closing the wealth gap

- Seek out financial education specifically addressing wealth-building for your demographic

- Consider pooling resources with family members to make larger investments possible

- Focus on acquiring assets that generate passive income rather than just savings

Alternative Investment Strategies for Building Wealth in 2025

You don’t need to be rich to invest beyond basic stocks and bonds anymore. New platforms let you buy small pieces of real estate, artwork, or businesses that were once only open to wealthy people. These different investment types often move in different patterns than the stock market, which can protect your money when stocks drop.

Some alternatives like farmland or certain real estate investments have beaten traditional stocks over time. Technology has made these options easier to access with just a few hundred dollars. The key is adding these choices carefully to create a more stable path to growth.

Tips:

- Start with small positions in alternative investments to learn how they work

- Use platforms that offer fractional ownership to diversify across multiple alternatives

- Balance higher-risk alternatives with stable investments for a healthier portfolio

- Research the fee structure carefully – some alternatives have hidden costs

- Consider the liquidity timeline – how quickly you can access your money if needed

- Join online communities where everyday investors share experiences with alternatives

The Vanishing Middle Class: Structural Changes in the Economy

The middle class keeps shrinking, dropping from 61% of Americans in 1971 to just 51% today. Jobs that once supported middle-class families have disappeared as companies move work overseas or replace people with technology. What’s left are mainly high-paying jobs needing advanced degrees or low-wage service jobs with little security.

Where you live matters more than ever, with some cities offering opportunity while others fall behind. This split creates a “barbell economy” with growth at the top and bottom but little in between. These changes make climbing the economic ladder much harder than it was for previous generations.

Tips:

- Develop specialized skills that are harder to automate or outsource

- Consider relocating to areas with stronger job markets and lower living costs

- Pursue education strategically, focusing on fields with proven return on investment

- Build multiple income streams to create your own economic safety net

- Look for opportunities in growing “middle-skill” fields like healthcare tech and specialized trades

- Network intentionally with people in industries showing growth and stability

“Stressflation”: When Inflation Meets Financial Anxiety

When prices rise while your mental health falls, you’re facing “stressflation.” This double threat hits hardest when everyday items cost more but your pay stays the same. Many people skip therapy or medication because they can’t afford both mental healthcare and basic needs.

The worry about rising costs actually makes smart money moves harder just when you need them most. People under financial stress often make short-term choices that hurt them long-term. Breaking this cycle means finding ways to protect both your money and your mind. Taking care of your mental health isn’t a luxury – it’s essential for financial success.

Tips:

- Use free mental health resources like community centers and employer assistance programs

- Practice the “24-hour rule” before making any stressed financial decisions

- Create an inflation-adjusted budget that acknowledges the reality of rising prices

- Find low-cost stress relievers that work for you – exercise, nature, or creative outlets

- Connect with others to share resources and emotional support during tough economic times

- Focus on what you can control rather than global economic factors beyond your influence