I’m 39 and Haven’t Worked in 3 Years: The Truth About Early Retirement Nobody Warns You About

On a sun-drenched Tuesday morning, the silence in Lucas’s paid-for house is absolute; it’s the kind of quiet he used to dream about, a stark contrast to the open-plan office chaos that once defined his days.

Three years ago, at 36, he walked out of his high-stress tech job for the last time, marking the finish line and triumphant culmination of a decade spent channeling a huge portion of his income into a meticulously managed investment portfolio.

That first taste of freedom was euphoric—a “sugar rush” of well-being where the boundless leisure time he had coveted for so long was finally his—but that rush fades; the silence now often feels like a void, and the boundless time has morphed into an “uncharted territory,” an unstructured expanse that can feel like an “existential vacuum”.

The Million-Dollar Mirage: When the Numbers Betray You

The foundation of the FIRE movement is mathematical certainty. Adherents believe that with the right savings rate and a safe withdrawal strategy, they can build an unshakeable financial fortress. Yet, this fortress is far more fragile than its architects admit.

It’s a high-stakes gamble against the unpredictable forces of market timing, human longevity, and the ever-rising cost of staying healthy.

The Tyranny of Timing (Sequence of Returns Risk)

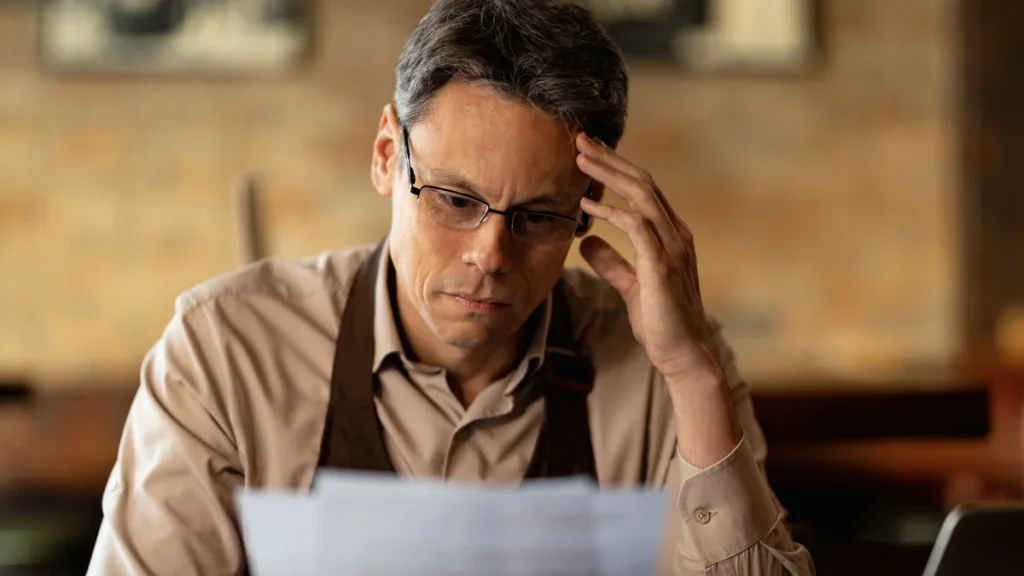

In his first year of retirement, the market dropped 15%. This wasn’t a theoretical dip on a quarterly statement; it was a visceral threat to his entire life plan. To cover his living expenses, he had to sell assets at a loss, a cardinal sin for any investor, but a potentially catastrophic one for an early retiree.

This experience was his brutal introduction to sequence of returns risk—the outsized danger that poor market returns in the early years of withdrawal can pose to a portfolio’s longevity.

The order in which one experiences investment returns matters immensely when they are drawing down their assets. Consider two hypothetical retirees, each starting with a $3 million portfolio and withdrawing $150,000 a year, adjusted for inflation.

For an early retiree with a potential 40- or 50-year time horizon, this risk is magnified exponentially. To mitigate this, financial planners recommend strategies to avoid selling assets in a downturn.

One of the most effective is the “bucket strategy,” which involves maintaining a cash reserve of one to three years’ worth of living expenses in stable, liquid accounts. This buffer allows growth-oriented investments to recover from market slumps without being depleted to pay for immediate needs.

The Healthcare Chasm

The Tyranny of Timing (Sequence of Returns Risk)

Consider two retirees with $3M portfolios, withdrawing $150k/year (inflation-adjusted). Both average 7% annual returns over 25 years.

- Scenario: -10% returns for the first 4 years.

- Outcome: Runs out of money in year 19!

- Scenario: -10% returns for the last 4 years.

- Outcome: Finishes with over $6.4 million!

The Healthcare Chasm

| Metric | Estimated Cost (2025) | Notes |

|---|---|---|

| Avg Monthly ACA Premium (Individual, age 40) | $621 | |

| Example High vs. Low-Cost State | $1,157/mo vs. $373/mo | (Vermont vs. New Hampshire) |

| Projected Total Premium Cost (Age 39 to 65) | ~$194,000 | (Decades of private insurance) |

| Fidelity’s Projected Lifetime Healthcare Costs (Post-65, Per Person) | $172,500 | (After Medicare eligibility) |

| Total Estimated Healthcare Burden (Pre- and Post-Medicare) | ~$366,500 | (Excludes long-term care!) |

The Slow Burn of Inflation and Longevity

Every trip to the grocery store is a psychological grind. Watching the price of everyday goods creep up is a constant reminder that my nest egg is a finite resource battling the relentless erosion of inflation.

A traditional 20- or 30-year retirement is a well-studied financial problem. A 50-year retirement—leaving work at 40 and living to 90—is a different beast entirely. The longer the timeline, the more devastating the compounding effect of inflation becomes.

The Great Unraveling: Who Are You Without Your Job Title?

The financial calculations of early retirement, however complex, are at least tangible. Far more disorienting are the internal challenges—the slow, quiet unraveling of an identity that was, for decades, inextricably linked to a career.

The Ghost in the Machine (Loss of Identity & Purpose)

At social gatherings, the dreaded question inevitably comes: “So, what do you do?” His answer—”I’m retired”—hangs in the air, feeling both alienating and incomplete at age 39. For years, his professional title was a shorthand for his identity, a source of validation and self-worth.

Without it, he felt like a ghost, defined only by what he no longer did. Psychologists confirm that this is a common and profound challenge. Work provides far more than a paycheck; it offers a daily structure, a set of goals, a social context, and a sense of status.

When this framework is abruptly removed, it can leave a void that many are unprepared to fill, leading to feelings of being “rudderless” or “useless”. This loss of a work-related identity can trigger a significant decline in mental health, as the very meaning of self requires re-evaluation and readjustment.

The first year was a blur of liberation. He traveled, tackled home renovation projects, and reveled in the novelty of weekday freedom—the classic retirement “honeymoon phase”. But in the second year, a creeping disenchantment set in.

This trajectory maps perfectly onto the “sugar rush” and “crash” phenomenon observed by researchers. The initial high of escaping work-related stress gives way to a sharp decline in happiness a few years later. This crash is a predictable identity crisis.

The Shadow in the Room (Depression & Anxiety)

It is difficult to admit, especially when you are supposed to be “living the dream,” but the past year has been a struggle with the shadows of depression and anxiety. I have often felt unmotivated, overwhelmed, and adrift, emotions that feel shameful and deeply isolating when the world sees you as having won the game of life.

My experience is not unique. A 2024 report from the Transamerica Center for Retirement Studies found that 24% of retirees often feel anxious and depressed, and 27% often feel unmotivated and overwhelmed.

Research also reveals a crucial nuance: the psychological impact of retirement heavily depends on the reason for it.

The Quiet Epidemic: Adrift in a World That Still Works

Perhaps the most insidious and least-discussed challenge of early retirement is the profound social dislocation it creates.

By stepping off the conventional career track decades ahead of schedule, you risk stranding yourself on an island of leisure while the rest of the world sails on with the tides of work and family life.

An Island of Leisure (Loneliness & Social Isolation)

His social life has slowly drifted away. His friends are still deep in their careers, navigating promotions, deadlines, and the daily grind of raising school-aged children. His weekday invitations for lunch or a hike are met with well-intentioned but unavailable replies.

He is living in a different reality, and the chasm is growing. The casual friendships forged in the workplace, which formed a significant part of his social fabric, have naturally faded without the daily reinforcement of shared projects and coffee breaks.

This personal feeling of isolation is a symptom of a much larger public health crisis. A 2024 national poll on healthy aging found that one in three adults aged 50-80 experiences loneliness, with rates even higher for those in the 50-64 age bracket.

The health consequences are dire; the U.S. Surgeon General has warned that the mortality impact of social isolation is equivalent to smoking 15 cigarettes a day. Early retirement can inadvertently place one in a high-risk demographic for this quiet epidemic.

Too Close for Comfort (Shifting Dynamics at Home)

The transition also brought unexpected friction to his relationship. His partner still works, and the imbalance in their daily schedules, free time, and household responsibilities created new and unspoken tensions.

After years of living parallel lives defined by separate workplaces, their constant proximity required a difficult period of renegotiating personal space, routines, and expectations.

Conclusion: Beyond the Balance Sheet: The Quest for ‘Net Fulfillment’

His third year of retirement began with a crisis. The loneliness, boredom, and anxiety had coalesced into a heavy weight. He had achieved the goal but lost the plot. It was then that he realized he had to stop mourning the life he thought he wanted and start actively building one that had meaning.

The turning point came when he encountered the concept of maximizing “net fulfillment” rather than just “net worth,” a term articulated by fellow early retiree Brandon Ganch, who regretted the years of extreme frugality that left him and his wife isolated and unhappy.

This idea reframed his entire perspective. Financial independence wasn’t the goal; it was the tool. The real objective was to use that tool to build a rich, connected, and purposeful life.

This realization led to a series of practical, intentional steps to rebuild his “life portfolio.” Supported by expert advice and the experiences of other retirees, he began to find his footing: Finding Purposeful “Work”: He took a part-time job at a local bookstore.

This “Barista FIRE” approach wasn’t about the modest income; it was about the structure, routine, and daily social interaction he had desperately missed. For others, this might mean starting a small consultancy or a passion project.

Rebuilding Community: He made a conscious effort to build new social networks outside the context of his old career. He joined a local hiking club, started volunteering at an animal shelter, and found an online Meetup group for other early retirees in his area. These communities provided connection with people who understood his new life stage.